The $3 Million Question

Visible Wealth vs Invisible Wealth

Financial debates are fascinating because the math is usually easy and the psychology is usually hard. Some can be settled with a calculator and simple Excel formulas. The tricky part is that for every ounce of arithmetic, there is a pound of preference.And those preferences boil down to nature, nurture, and a whole slew of factors that make money one of the most emotional topics to discuss.

Some of my favorite financial bloggers set off a debate when Nick Maggiulli tweeted this:

Why is a $3M home a status symbol but a $3M portfolio isn’t?

How can someone value “looking wealthy” over having more financial freedom?

Makes zero sense.

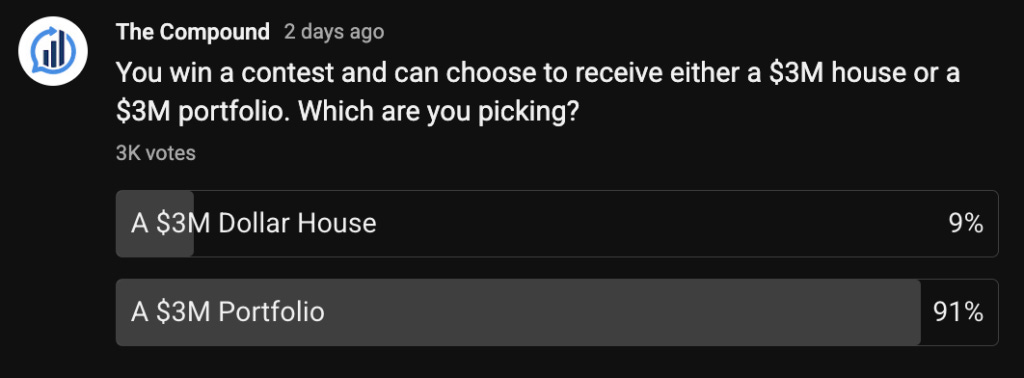

Nick’s colleagues Michael and Ben also posted a poll on their podcast asking the same question, and here was the breakdown:

The uncomfortable truth is that visible wealth and invisible wealth scratch very different psychological itches.

There is no doubt the $3M portfolio offers much more flexibility and is the sensible choice. The crowd polled here is also a group of personal finance nerds like me, so take this with a grain of salt. I think in real life the survey would not look so lopsided.

Part of the tension here is that homes are visible wealth and portfolios are invisible wealth. One gets you compliments at dinner parties. The other buys you optionality that no one can see. Humans have always been pulled toward the visible scoreboard, even when the invisible one matters more.

So much of this comes down to the utility and happiness each option can bring you. If the $3M house allows you to gather frequently with your closest group of family and friends, utility is off the charts. If the $3M portfolio allows you to take amazing vacations to create memories or give to causes that mean the most to you, utility is off the charts.

For those thinking the $3M portfolio is a slam dunk, it is worth remembering that many retirees struggle to spend their hard earned millions. Pretending you live on a fixed income when you have a 7 figure portfolio might be equally as sad as the $3M mansion that sits vacant.

Nassim Taleb says:

I will set aside the point that I see no special heroism in accumulating money, particularly if, in addition, the person is foolish enough to not even try to derive any tangible benefit from the wealth (aside from the pleasure of regularly counting the beans).

It is also fascinating to me that among my friends, I usually know whether they own or rent their home. I could probably guess, within a reasonable range, how much their home costs. None of this is judgment. Real estate is simply an easy yardstick to use, no matter how flawed it may be.

But for that same group, it is nearly impossible to know whether their brokerage and retirement accounts are closer to five figures or seven.

The honest answer is that this question is heavily situation and age dependent. In your accumulation years, financial flexibility tends to dominate. Later in life, the emotional pull of space, proximity, and gathering places often grows stronger. The right answer at 35 may not be the right answer at 55.

For what it is worth, today I would take the $3M portfolio. I would enjoy a meaningful portion of it now, creating memories with the people who matter most to me.Then, I’d aim to grow the account, but only until age 50. From there, I’d work on spending it down.

I borrowed this idea from Die With Zero, where age 50 is described as Peak Health and Wealth.. 50 is often identified as a time when individuals have the highest combination of accumulated assets and, for many, peak physical capability to enjoy them.

If you asked me this question at age 50, maybe I would take the $3M house because I would have visions of hosting kids and grandkids in a larger home.

You’re allowed to change your mind. It’s not against the rules.