The Tables Turn

What happens when the stocks that carried the market become the ones dragging it down

The stock market has treated us very kindly for quite some time. Despite plenty of hiccups and scares along the way, the market has been resiliently moving higher for about 17 years, which is when we had our last real recession.

The main gripe the nitpickers have had is over a sizable chunk of those years, the stock market has become quite concentrated to some large winners. It drove the stock pickers and portfolio managers insane because the guy or gal who invested their entire portfolio in a S&P 500 index fund outperformed the professional in lots of those years.

But this was never a promise or a golden rule. Here’s Paul Kedrosky earlier this week:

Year-to-date, the S&P 500 index is down 7%, but that headline hides record concentration. The “Hateful Eight” — the Mag 7 + Oracle that drove index gains for the past two years — account for 85% of the year-to-date drawdown, subtracting roughly 576 points. The other ~490 companies collectively added about 100 points.

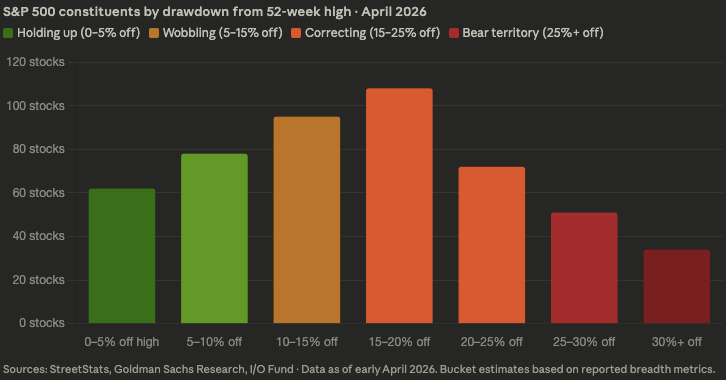

For much of the recent market run, a small group of mega cap tech companies did most of the heavy lifting. Now we are seeing the flip side of that. Those same companies are weighing on the market because they make up such a large portion of the indexes.

The biggest names leading the pullback are the usual suspects: Microsoft, Nvidia, Apple, Google, Amazon, Meta, Tesla, and Oracle.

And it doesn’t stop there. There’s plenty of wreckage down 20% or worse.

Moments like this can be tempting to bottom fish. I’m normally not a fan of bottom fishing because the fish on the bottom are generally there for a reason. But we sometimes have opportunities in front of us where incredible businesses are being victimized by indiscriminate selling, the health of the business be damned.

If you’re loading your tackle box and getting ready to cast a line into the wreckage, here are a few things to consider.

You don’t need to bet the farm on a single name. Software has been the epicenter of the atom bomb that detonated. Iconic names like Salesforce, Adobe, and many others are taking it on the chin. It’s tempting to buy one because the drawdowns in these names are investors thinking their competitive moats have had an unpatchable hole blown through them.

But what if they’re right and the fear was warranted? What if you’d prefer to say “I think the sector as a whole is way oversold and I’d like to participate in the bounceback?”

In that case, you could buy a name like IGV which holds names like Palantir, Microsoft, Oracle, Salesforce, and Palo Alto Networks. Here’s how Josh Brown thought about the purchase:

I took a shotgun approach. I know all the big names in this ETF generally but I don’t spend a ton of time on each of them every quarter or think I have an edge over the folks who do. I basically just wanted to buy pure, unadulterated panic at the close of trading last week. So I did. IGV is the iShares Expanded Tech-Software Sector ETF and it’s in a 30% drawdown since October.

Know whether you’re a trader or investor. If you’re a trader, you should have some sort of defined risk management strategy, whether those be stop losses or something else. If you’re an investor, you don’t need to back up the truck right from the get-go.

The label matters more than people realize. Investors who truly know what they are don’t need the market to cooperate right away. They need the company, or the index, to be worth more in ten years than it is today. That conviction is what separates the people who look back on moments like this as opportunities from the ones who remember them as the time they panic-sold into the bottom.

The wreckage underneath the surface that we looked at earlier tells a sobering story. But the thing is a market where the majority of stocks are already down 15, 20, 25 percent from their highs is a market that has already done a lot of its damage. The headlines will catch up eventually, but by then the prices will have moved. That’s always been the cruel joke of investing. The best time to act rarely feels like the best time to act.

Patience & stubbornness are close cousins. In The Money Game, George Goodman says “If you don’t know who you are, the stock market is an expensive place to find out.”

The market is sneakily skilled at finding the gap between what you said you believed when things were calm and what you actually do when things get uncomfortable. Risk tolerance only shows up in the heat of the moment. Most people discover they had a higher tolerance in theory than they do in practice. As Mike Tyson put it, “everybody has a plan until they get punched in the mouth.”

The S&P 500 index eventually gets back to even because dead weight gets removed and replaced. Individual stocks don’t get that edit. Cisco peaked in March 2000 at around $80 a share and it only recently got back to those same levels.

Nobody rings a bell at the bottom. The market doesn’t send you a calendar invite when the coast is clear. What it does eventually is reward the people who knew what they owned, knew why they owned it, and didn’t let a few ugly headlines talk them out of it. It’s one of those “simple, yet difficult” things to do.